After working over 40 years and paying National Insurance every week, you now get the full State Pension. You’d think that would make life a bit easier.

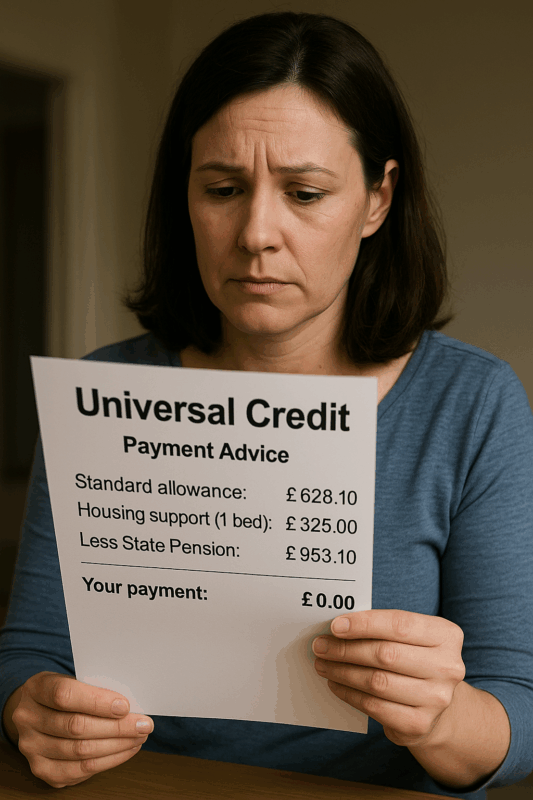

But here’s the catch — under Universal Credit rules, your state pension is treated as household income, not your own.

That means your partner, who’s younger and unable to work due to health problems, gets no support at all. Universal Credit deducts every penny of myyour state pension from what you’d otherwise receive.

Before May 2019, couples where one partner had reached State Pension age could claim Pension Credit and get vital top-up support.

But since the rule change on 15 May 2019, new “mixed-age” couples are forced onto Universal Credit instead — and they get nothing if one partner’s pension pushes them over the limit.

In other words, if one of you is on a State Pension and the other can’t work, you’re told to live on one pension. No top-up. No help. No fairness.

Universal Credit isn’t looking so “universal” anymore.

It’s time for this rule to be reviewed — because a pension should be a reward for work, not a reason to take support away.

I’m not criticising people who work hard at the DWP, but the system itself needs a serious rethink.

How can it be right that someone’s earned pension cancels out their partner’s need for basic support?

It’s time policymakers reviewed this rule — because fairness shouldn’t stop at State Pension age.

If you or someone you know has been affected by unfair Universal Credit or Pension Credit decisions, Golden Shield Consumer Services can help you understand your rights and challenge unfair outcomes.

🔗 Visit www.goldenshieldservices.co.uk/free-case-review for a free initial review.

#UniversalCredit #StatePension #FairnessForCouples #GoldenShieldServices